BCG Is a Thought Leader in the Pension De-Risking Industry

By clicking on any of the articles below, you can request a PDF.

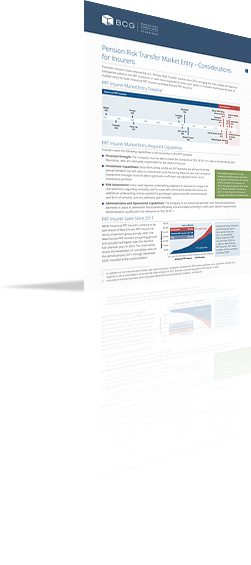

Pension Risk Transfer Market Entry – Considerations for Insurers

Fourteen insurers have entered the U.S. Pension Risk Transfer market since 2014, bringing the total number of insurance companies active in the PRT market to 21 with more expected to enter soon. This article shows a timeline that depicts the year of market entry for both Historical PRT Insurers and New Entrant PRT Insurers and discusses the capabilities insurers need to be successful in the PRT business. The article also breaks out the pension group annuity sales and new contracts sold between Historical PRT Insurers and New Entrants since 2011, provides a recent market size snapshot of the U.S. defined benefit market and highlights that despite another big year for the PRT market being underway in 2024, technical impediments continue to be a hurdle for some plan sponsors.

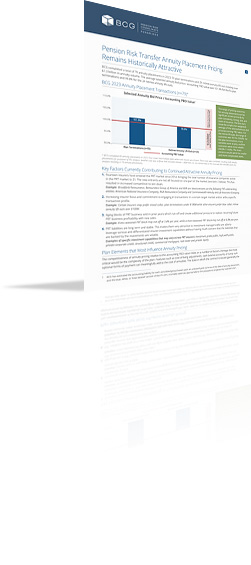

Pension Risk Transfer Annuity Placement Pricing Remains Historically Attractive

BCG completed a total of 79 annuity placements in 2023, 55 plan terminations and 24 retiree annuity lift-outs totaling over $1.3 billion in annuity volume. The average selected annuity bid price / accounting PBO value was 101.9% for the 55 plan terminations and 99.8% for the 24 retiree annuity lift-outs. This article summarizes the pricing outcomes for its 2023 completed PRT annuity placements and highlights the key factors that are currently contributing to continued attractive annuity pricing. The article also discusses plan elements that most influence annuity pricing and plan sponsor action items.

BCG Thought Leadership 2023 Roundup, Three Pension De-Risking Market Predictions for 2024 and A Tip of the Hat

In this first featured article of 2024, we are taking a look back at the articles, surveys, spotlight series Q&A interviews, etc. that BCG authored and/or collaborated on in 2023 in its highly followed industry newsletter, The BCG Pension Insider. We also make three pension de-risking market predictions for 2024 and tip our hat and say thank you.

The Critical Role LDI Plays to Lock In DB Plan Funded Status Inflection Points

There was a significant uptick in interest from plan sponsors to de-risk or terminate their defined benefit plan when the 10-Year Treasury briefly hit the 5% mark in October. While many plan sponsors seized the opportunity, others were not prepared to lock in this funded status inflection point. They did not have a liability driven investment (LDI) strategy in place to hedge their liability and to preserve their plan's funded status. This article encourages plan sponsors with no current LDI strategy to put in place an LDI strategy, so their DB plan is positioned to lock in funded status inflection points when they happen as the “windows” for optimal de-risking are often fleeting.

Two Foundational Questions that Demand C-Suite/Board Attention

Significant funded status improvement for defined benefit pension plans has caused many plan sponsors to shift away from return seeking assets in favor of more complete liability hedging. It has also led plan sponsors to initiate the process to determine its preferred pension endgame strategy whether it be plan termination, plan hibernation or something else. With this backdrop in mind, this article identifies two foundational governance/strategy questions that demand C-Suite/ Board attention as well as additional governance/strategy questions that can help plan sponsors avoid potential conflict of interest issues surrounding the future direction of their DB plan(s).

My Defined Benefit Plan is Overfunded on a Plan Termination Basis – Now What?

This article is a call to action for plan sponsors with fully funded or even overfunded defined benefit plans on a plan termination basis to expand liability driven investing (LDI) implementation to lock in funded status, evaluate desired pension plan “endgame” strategy, and initiate customized buyout price monitoring so they are prepared to take action when the right conditions are met. A plan sponsor “should do” list is provided as well as a step-by-step guide to prepare the asset portfolio for plan termination and a summary on what plan sponsors can do with a pension surplus.

Plan Sponsors Beware – Participating Group Annuity Contracts in DB Plans

This article discusses participating annuity contracts in DB plans, and why plan sponsors need to beware if their plan holds an open or on-going participating group annuity contract, since this will complicate de-risking and plan termination. This article includes a worked example, discusses why plan sponsors entered into participating contracts and what can be done. It is crucial that the plan sponsor understands early on the implications of discontinuing or terminating a participating contract on the ultimate cost of plan termination, and/or the cost implications that can make a plan termination prohibitively expensive.

Fiduciary Considerations in the Context of IB 95-1

This article discusses fiduciary considerations in the context of Department of Labor Interpretive Bulletin 95-1 (“IB 95-1”), including a framework a fiduciary should consider in selecting an annuity provider and contract in a pension risk transfer annuity buyout. The article also discusses Administration, its relevance under IB 95-1 and takes a deeper dive into key administration factors, including major administration considerations and why they are important.

Pension Risk Transfer Market Observations in Five Charts

With many plan sponsors and advisors considering what pension de-risking strategy may be best for their defined benefit plan in the current environment, this article identifies and explains important pension risk transfer (PRT) market observations in five charts.

Charts taken from BCG Pension Risk Consultants I BCG Penbridge’s (BCG) PRT Index charting tool, which was established in 2011.

BCG Thought Leadership 2022 Roundup, A Look Ahead to How the Pension De-Risking Market is Evolving in 2023 and Beyond and A Big Thank You

In this special edition newsletter, we are taking a look back at the articles, surveys, spotlight Q&A interviews, etc. that BCG authored and published in 2022. We also offer a look ahead to how we see the pension de-risking market evolving in 2023 and beyond as well as a big thank you.

COVID-19 Pandemic and Future Pension Risk Transfer Mortality – What’s Next?

It goes without saying that the COVID-19 pandemic has significantly affected the world in all aspects of daily living. The impact on the insurance industry, and in particular pension risk transfer (“PRT”), goes beyond just the number of deaths that have occurred. This article focuses on the mortality impacts, both historically as well as what the future may bring, with a focus on potential impacts on insurers’ PRT business. It also addresses the additional information that PRT insurers are using and requesting in evaluating PRT transaction opportunities.

The UK Pension Market Crisis and Why the US Pension Market Is Different

When the tide goes out it becomes more dangerous to navigate a harbor as rocks and shoals are nearer a ship’s hull and threaten destruction. The financial market corollary is central banks draining liquidity and exposing financial institutions to potential demise. Monetary authorities are now in a tightening mode across the world. Institutions that do not have well designed asset-liability hedging strategies are in peril. Historic examples of flawed strategies include: the 2008 financial crisis, the 1998 Long Term Capital Management crisis, and the banking and savings and loan crises of the 1980s and 1990s. This paper describes UK pension plans use of leverage and how they became an early casualty in the current round of global monetary tightening. We also highlight key differences between UK and US pension markets and why it is critical during this period of Fed tightening/market volatility for plan sponsors and their advisors to continually be on the watch for attractive annuity pricing opportunities.

Technical Impediments to Pension De-Risking

The trend of increased pension de-risking has been clear over the last decade. 2021 was a record year in the annuity market, with over $38 billion of buyouts and buy-ins recorded. While continued busy years in the annuity market certainly lie ahead, there are technical impediments that some plans will face that will prevent them from taking de-risking action(s) while the iron is hot. Identifying and addressing these hurdles may allow for plan sponsors to optimally de-risk sooner rather than later, taking advantage of the attractive annuity pricing that so many other pension plans have benefited from in recent years. This paper identifies accounting considerations that may prevent pension plan sponsors from de-risking, and discusses steps to begin addressing these barriers.

Pension De-Risking – The Time for Plan Sponsor Action Is Now

A BCG special feature article in collaboration with BofA Global Research.

Defined benefit pension funds have always been an important source of demand for the bond markets (i.e., Treasury and Investment Grade Credit markets). With recent increases in Treasury rates and widening of investment grade corporate spreads, many DB plans are now at or near being fully funded. With the risk of recession on the horizon, and simultaneously falling Treasury rates, the time for plan sponsor action is now. In this article BCG in collaboration with BofA Global Research attempt to quantify what expected de-risking will mean for demand for Treasury and Investment Grade Credit bonds from both long duration/LDI and PRT strategies.

Factors Determining Whether an Insurer Will Decide to Bid on a PRT Annuity Placement

Why is it that some defined benefit annuity placements will have only one or two pension risk transfer (PRT) insurers bidding on a particular opportunity, while others may have half a dozen or more? One critical factor is the size of the annuity purchase. This paper explores the factors, beyond just the size of the purchase, that will determine number of bidders.

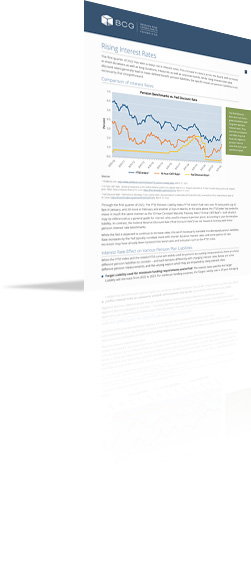

Rising Interest Rates

The first quarter of 2022 has seen a steep rise in interest rates. This increase in rates is across the board, with increases in short durations as well as long durations, treasuries as well as corporate bonds. While rising interest rates (aka discount rates) generally lead to lower defined benefit pension liabilities, the specific impact on pension liabilities is not necessarily that straightforward.

BCG Thought Leadership 2021 Roundup and A Look Ahead to How the Pension De-Risking Market is Evolving in 2022 and Beyond

In our first newsletter featured article of 2022, we are taking a look back at the articles, surveys, spotlight Q&A interviews, etc. that BCG published in 2021. We also offer a look ahead to how we see the pension de-risking market evolving in 2022 and beyond.

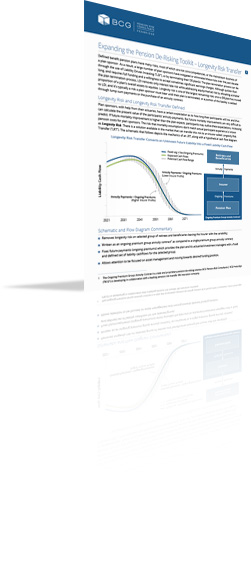

Expanding the Pension De-Risking Toolkit — Longevity Risk Transfer

Plan sponsors, with help from their actuaries, have a certain expectation as to how long their participants will live, and thus can calculate the present value of the participants’ annuity payments. But future mortality improvements are very difficult to predict. If future mortality improvement is higher than the plan expects, participants may outlive these expectations, increasing pension costs for plan sponsors. The risk that mortality assumptions don’t match actual participant experience is known as Longevity Risk. There is a solution available in the market that can transfer this risk to an insurer called Longevity Risk Transfer.

Addressing Alternative Assets in Defined Benefit Plan Terminations – Considerations for Plan Sponsors

With larger and more complex defined benefit (DB) plan terminations on the rise and continued growth in terminations in the U.S. pension risk transfer (PRT) market expected over the next decade, DB plan sponsors need to consider best practices for disposing their plan’s illiquid, alternative assets (e.g., private equity, real estate, hedge fund investments), if any, in the most cost-effective and timely manner.

Is your Defined Benefit plan hard frozen? If so, chances are it has been hard frozen for some time. The question is: What are you waiting for?

Roughly 40% of all ERISA qualified defined benefit (DB) plans over $10M in assets are hard frozen, meaning there are no further benefit accruals. Many of these plans have been hard frozen for some time. In fact, 81% of hard frozen DB plans have been frozen for five years or more, and 54% have been frozen for 10 years or more. This paper raises two key questions for plan sponsors of hard frozen DB plans and identifies key considerations for plan sponsors whose DB plan has been frozen for an extended period of time.

Highlights from BCG’s 2021 Survey of Asset-In-Kind Practices of Annuity Providers

It is important for plan sponsors and their advisors to understand the practices of annuity providers related to asset-in kind (AIK) transfer arrangements for pension risk transfer annuity buyouts, so that they can prepare the asset portfolio and optimally carry out the transaction. Here, we present some highlights from BCG’s 2021 Survey of Asset-In-Kind Practices of Annuity Providers. Notably, 17 of the 18 currently active PRT annuity providers participated in the survey.

Pension Risk Transfer Annuity Placement Pricing is Better Than Ever – Will it Last?

BCG completed a total of 53 annuity placements in 2020, 42 plan terminations and 11 retiree annuity lift-outs totaling over $1 billion in annuity volume. The average selected annuity bid price / accounting PBO value was 101% for the 42 plan terminations and 94% for the 11 retiree annuity lift-outs. These percentages are not typos! This paper explores the current state of the US pension risk transfer market, specifically as it relates to three factors that are currently contributing to exceptional annuity pricing.

Liability Driven Investing When Plan Termination is the “Endgame” Objective

As a defined benefit (DB) plan sponsor, it is imperative you work with advisors who are aligned with your objectives and understand your goals and time horizon. It is also imperative to work with advisors who understand the important role liability driven investing (LDI) plays when plan termination is the endgame objective. This paper explores the importance of employing a custom liability benchmark , aka “Custom LDI,” based on a plan’s liability and how a customized LDI-PRT approach provides the most comprehensive solution.

Pension De-Risking – A Recommended First Step

This short paper helps defined benefit plan sponsors answer the question, “How do I get started down my plan’s de-risking path?”. An illustrative pension de-risking roadmap captures steps that can be taken from a pension liability perspective and from a pension asset perspective. Further discussion focuses on BCG’s recommended first action for any plan sponsor which is to evaluate their DB plan’s expenses, i.e., “What are my plan’s holding costs?”.

Major Insurers Flock to U.S. Pension Risk Transfer Market

Prior to 2014, there were eight insurers in the U.S. pension risk transfer (PRT) market that were continuously active for many decades, with the longest tenured insurer being MetLife who entered the PRT business in 1921. That’s right -- 100 years ago! Following MetLife, while other companies entered and exited the market, seven insurers joined and remained active in the PRT market at different points over the ensuing 60+ years. Read this short paper to better understand how the increasing numbers of insurers in the PRT market is impacting pricing and market capacity.

“Check, Please!”: The Importance of Administration in the Selection of an Annuity Provider

This white paper provides a comprehensive framework for how fiduciaries should examine administrative considerations in the Information Age. It explains why a review of insurers’ administrative capabilities and practices is crucial for a fiduciary selecting an annuity provider, how technological changes (e.g., cybersecurity threats) have made it even more critical, and what key aspects of insurers’ administration a fiduciary should focus on.

Survey of Assets In Kind Practices of PRT Providers

Summary results and key observations from Penbridge’s 2016 survey addressing insurers’ assets-in-kind (AIK) transfer practices. 100% of insurers responded to the request to participate. It is important for plan sponsors and their advisors to understand the practices of insurers related to AIK transfer arrangements for annuity buyouts so that they can prepare the asset portfolio and carry out the transaction with optimal efficiency.

Defined Benefit Expense Survey and DB Expense Benchmarks Reports

Summary results of the first industrywide survey to capture all the costs associated with maintaining a U.S. corporate defined benefit (DB) plan. The survey is intended to give plan sponsors access to unbiased and comparable expense data to help them make informed decisions involving the costs of their DB plans. Set up as a rolling survey, participating sponsors receive, at no charge, a customized DB Expense Benchmarks Report. To view a sample Benchmarks Report, click here. To participate in the survey, click here.

Preparing Assets for Pension Risk Transfer

Plan sponsors preparing for PRT transactions need to position their assets to go through the process efficiently and with minimal asset liability management risk and cost. The first half of this paper presents the essentials of asset positioning for plans that are preparing for termination. The second half examines the growing practice of assets-in-kind transfers, drawing upon the results of a Penbridge survey of US insurers.

The Fiduciary’s Role in the Termination of Single Employer Defined Benefit Plans: A Practical Guide

While de-risking of defined benefit plans takes many forms, the most comprehensive set of actions involves termination of the plan and transfer of its liabilities to an insurer by purchase of an annuity buyout contract. This article by Ivins, Phillips & Barker and Penbridge Advisors sets forth in Part I a checklist of plan sponsor and fiduciary actions. Part II expands on the fiduciary’s risks and responsibilities in bringing the termination to a close.

The Case for Pension Risk Transfer

As US corporate plan sponsors continue to find less appeal and more challenges with their defined benefit plans, they will explore more ways to reduce or eliminate the DB plan risks they hold. And as they find the barriers to transaction dropping, the upshot will be a huge increase in PRT deals.